Table of Contents

It is possible to get additional gap insurance coverage on top of your existing policy, but it’s not required. Gap insurance will pay off your remaining balance if your automobile gets stolen or written off as a total loss. Whereas, Gap insurance does not take care of any damages to your vehicle or any other person’s property, as well as cover any injuries, greater than average financing gaps, oversights in payments, regular upkeep tasks, or your excess.

There are many companies offering gap coverage, including dealers, lenders, and insurers, so make sure to inquire about it when purchasing car insurance. Keep on reading to discover the particulars of gap insurance, the instances in which gap insurance will pay do not, claim filing procedures, and the policyholder’s responsibility in instances wherein their automobile suffers complete loss damage.

What is the process for using gap insurance?

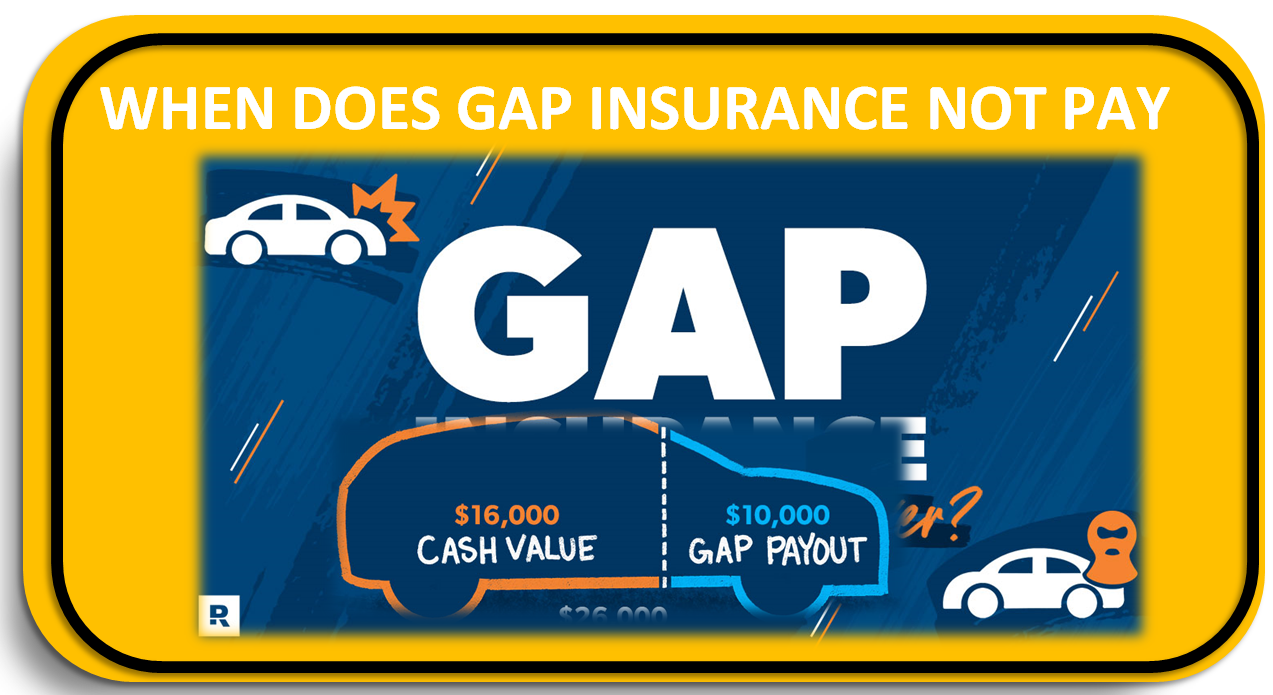

Gap insurance is a supplementary insurance policy that can protect you when purchasing a vehicle with a loan or lease. If your vehicle is rendered a total loss due to an accident and you owe your lender more than the car’s actual cash value (ACV), gap insurance can cover the difference.

For instance, if you have a loan of $20,000 and your car is stolen and valued at $15,000, with gap insurance, also known as loan/lease payoff coverage, your insurance would cover the remaining balance of $5,000 with your lender. If you do not have gap insurance, you would have to pay the $5,000 on your own to pay off the loan balance. Clearly, even if one is out of the car, the financial obligation to pay for the lease or loan continues as well.

While gap insurance is, in most cases, optional, it is mostly a requirement for leased vehicles. This type of insurance can either be provided within the lease agreement or have to be purchased separately. The lender or the dealership usually offers it, but purchasing it through your car insurance may also be more affordable.

Look through your lease agreement closely to see if the “gap waiver” charge is there.

Seven Cases Where Gap Insurance Does Not Pay Out

Gap insurance does not pay out in every situation, however. Here are seven things gap insurance does not cover.

1. Damages from accidents and injuries on the body

The insurance gap does not take responsibility for paying damages from an accident, irrespective of who caused it. This covers injuries to you and your passengers, the other driver and their passengers, your vehicle damages, and anyone’s property damages.

2. Negative equity

People purchase brand new vehicles lots of time while having existing loans for older cars. Negative equity will more than likely not be covered by gap insurance if you are rolling over residual money from existing loans or leases.

3. Other optional coverages and extended warranty

Optional coverages, Maintenance or extended warranty restrictions are inclusive in your initial loan amount. Gap policies are designed to cover the balance of the car loan and leave out the non-base coverages that are included in the base loan.

4. Regarding car payments that are not made

You can miss a monthly sitting due to suffering from disability, death, injury, or even unemployment. Gap insurance covers missed payments or fees that you may have accumulated if your car was destroyed after being involved in an accident.

5. Common upkeep

Typically, gap insurance and a standard car insurance policy will not cover normal wear and tear on your automobile. There can be optional mechanical failure coverage in some policies. However, it won’t cover failure in Maintenance. Furthermore, gap insurance companies also will not cover it.

6. Your deductible for collision and comprehensive coverage

You are likely to get in a car accident that forces you to exercise your comprehensive and collision coverages. Both of these have a deductible which is the amount towards fixing or replacing your vehicle that you pay.

Gap insurance will not cover the deductible from your comprehensive and collision insurance.

7. Surrendered value of the vehicle

Your vehicle is likely to depreciate in the fair market value after it gets into a damaging accident, but your car will not be a total loss. Even if your car is damaged in an accident later on, gap insurance will not cover the value received lower than the vehicle’s ACV. Moreover, gap insurance will not cover the amount you did not receive because of the car’s surrendered value.

Is Gap Insurance Necessary?

Buy gap insurance if you:

- Financed your new vehicle for 60 months and above

- Got a car lease that needs Gap Insurance

- Paid less than 20% on a vehicle purchase

- Acquired a vehicle that loses its value at a higher rate than most cars.

How to Make Use of Gap Insurance

Claiming gap insurance is simple. Depending on where you purchased your gap insurance, you are able to file a claim over the phone, online, or in person. Also, you will need documents that show the difference between the ACV of your vehicle at the time of the accident and the outstanding balance of your loan. This could include:

- A police report that states the specifics of the accident and the date of loss

- Loan or lease finance agreement that details how the loan terms have been financed

- The original MSRP, factory invoice or sales agreement, along with the purchase price of the car

- Loan statement that details how many payments you have made toward this loan and what your remaining balance is

- Settlement statement from the insurance that details the amount paid for the car’s ACV vs the amount the insurance is covering.

- A copy of the settlement check showing the amount paid to the finance company.

A claim would be easier to submit if gap coverage was included with the auto insurance, particularly if the insurance company dealt with the claim regarding the vehicle that was destroyed.

How Does the Insurance Company Value Your Vehicle for a Total Loss?

An auto insurance provider will consider a vehicle to be a total loss when repairs exceed the value of the car. Companies arrive at this number by something called a “total loss threshold,” which varies by state. Insurance companies employ two methods to determine this threshold.

Simple percentage threshold:

This applies to most other states where the vehicle is considered a loss when repair expenses go over a fixed percentage of the vehicle’s worth. Most use 70 to 75 per cent, and some use as low as 60 and as much as 100 per cent.

Formula for Total Loss (TLF):

The TLF computes the worth of the vehicle from two different perspectives: the worth of the vehicle in terms of spare parts (that is, what it can be sold in damaged condition) and the expense to repair the vehicle, in comparison to its actual market value. For instance, If the vehicle’s salvage value is $800 and repair costs are $8,000, but the vehicle’s actual cash value is $10,000, it isn’t a total loss. But if the repair costs were $9,500, it would be considered a total loss.

What are the reasons why ‘GAP Insurance’ will not pay out?

Your main motor insurer does not pay out

For a GAP Insurance policy to pay out, your primary insurer must settle your claim first. To reiterate, a vehicle’s insurance value must be paid for by the insurer. After that, the driver’s insurance will cover the remaining cost.

If your GAP claim can’t be filed, then your motor policy is not responsible for the settlement you have incurred with the motor policy.

Some reasons why your motor policy would not incur a cost include being negligent in leaving an unattended vehicle with the ignition running. Other examples range from drunk driving to using the vehicle for things like courier or taxi use, which are all prohibited.

You do not have an ‘insurable risk’ on the vehicle.

This implies that even though you took out GAP insurance, you do not stand to lose anything financially if the vehicle is damaged beyond repair.

A good example would be when you take out a GAP policy, but the vehicle’s ownership and finance documents are held by someone else.

Because the vehicle is not under your name, a loss claim cannot be made.

The vehicle is being used for certain commercial activities*

As with other insurance products, most GAP Insurance products do not cover some “commercial activities” with standard cover. This is particularly true for people who their motor insurer covers.

One type of commercial use that is frequently not included in the standard cover is hired and reward contracts. These can be taxi, private hire, courier, and chauffeur services.

Other areas of commercial work that might not be included would be driving maneuvers with teaching vehicles.

You are no longer making premium payments under the agreement

You could make any monthly payments for the GAP cover if you so wished. If you choose not to make any payments, then the cover will end.

You Change Ownership Or Dispose Of The Vehicle

The GAP cover will usually stop if you dispose of the vehicle or sell it. You may also notice this when changing the V5 ownership document within a family. For instance, if the father purchased the vehicle, he may give it to his son or daughter. The purchase invoice for the vehicle is in the father’s name. The change of keeper to his son or daughter means he could miss out on making a GAP claim.

It has already been used for cashing the benefit under claim

GAP Insurance can be described as only being available to cover specific loss circumstances ‘once only’. If you can successfully claim it in cash after the vehicle has been written off, that is the end of the policy.

This was the case last time I checked, too, so make sure to double-check and see if it allows you some leniency.

If the vehicle you replaced is different from the one you claimed with insurance, then you will also have to get a new GAP policy for this vehicle.

There is no financial GAP left to fill

Do keep in mind that GAP cover is meant to increase what the motor insurers pay you to close to what you spent on the vehicle. If, however, there is no ‘gap’ between what the motor insurers pay and the price you paid (if that is the value truly what you bought), then your cover has no difference to make up.

An additional case in which something like this may occur where there is no GAP is where your motor insurer does an automatic replacement on your behalf. Your car was new, and so is what your insurer replaced it with.

Your loss might not be something people experience very often, but if they do, you have nothing to worry about. Mostly, you will notice your GAP cover applied to your other vehicle without any fees.

Your GAP Insurance policy has been discontinued.

All GAP products have a period of cover. When the policy comes to an end, you usually cannot renew or get new cover as you have owned the vehicle for too long.

The decision on how long of a GAP insurance cover you wish to have on your vehicle s something you have to decide on at the initiation of the policy.

You do not have complete comprehensive insurance.

Most GAP policies will require that you are fully protected for the entire term. If you are only covered by third-party liability, then your motor insurer would not cover you for a fault claim or a stolen car. If your primary motor insurer does not pay, then you cannot claim any benefit on the GAP insurance.

Your car does not show in the Glasses Guide.

You may have heard of Glass Guide, as it is used by almost all insurers and motor dealers when determining the value of a vehicle. Many GAP products will not cover you if your vehicle is not listed in the Glasses Guide.

This is simply because GAP is meant to cover from the ‘write off’ value of the vehicle and upwards.

Without guide prices to estimate the correct write-off value, GAP Insurance underwriters are unable to determine the coverage values.

Learn More about :-

1 thought on “When Does Gap Insurance Not Pay”